Introduction

By automating your savings, you create a system that consistently transfers money to your savings accounts without requiring manual action, eliminating decision fatigue and emotional barriers to saving. This approach ensures regular contributions regardless of motivation levels, maximizes compound interest through timely investments, and builds wealth effortlessly through a “set it and forget it” approach that makes it significantly easier to reach your financial goals.

Financial success rarely happens by accident. The most effective way to build wealth is through consistent, disciplined saving and investing habits. However, relying on willpower alone makes it easy to forget or choose immediate gratification over long-term financial health.

This is where automation becomes your most powerful ally. By setting up systems that save and invest your money automatically, you remove the psychological barriers that prevent consistent saving and ensure your financial goals stay on track regardless of life’s distractions.

This guide will walk you through everything you need to know to create a personalized, automated savings system that works silently in the background while you live your life.

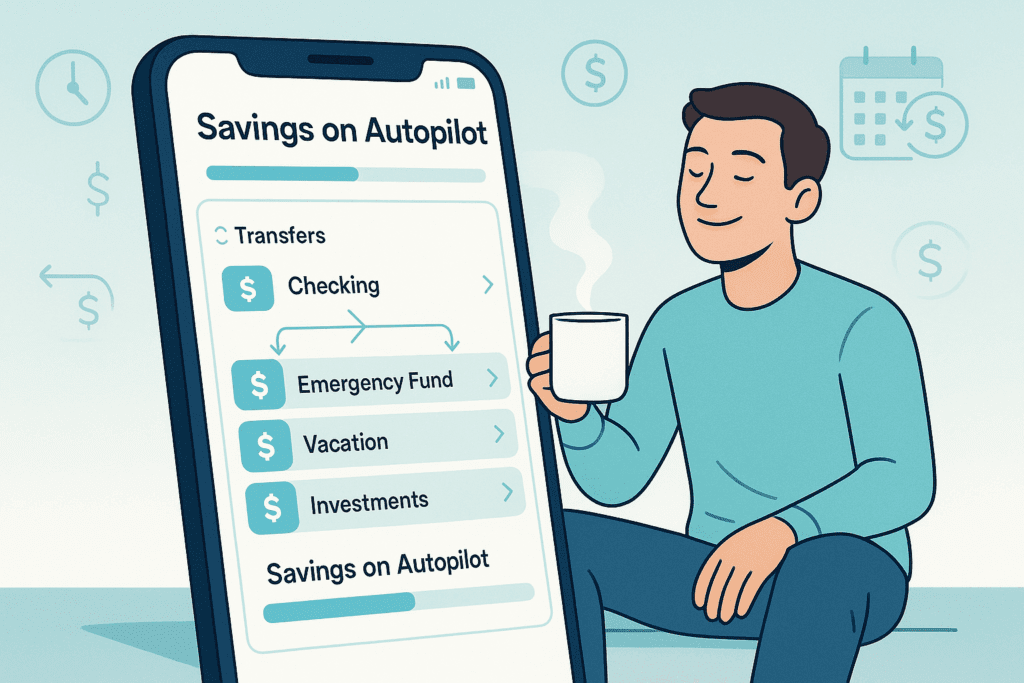

What is Savings Automation?

Savings automation is the process of setting up recurring transfers between your accounts, splitting direct deposits, or using apps that automatically move money into savings or investments based on predetermined rules. Once established, these systems work silently in the background, ensuring consistent progress toward financial goals without requiring constant attention or willpower.

Why Automate Your Savings?

Automating your savings offers several key advantages:

- Consistency: Ensures regular contributions regardless of memory or motivation

- Psychological benefit: Removes the emotional pain of actively transferring money to savings

- Efficiency: Eliminates decision fatigue and the need for repetitive financial tasks

- Compound growth: Maximizes returns through regular, timely contributions

- Error prevention: Reduces the risk of missed savings opportunities

- Budget management: Makes saved money “invisible,” reducing spending temptation

How to Automate Your Savings in 4 Simple Steps:

1. Split your direct deposit – Ask your employer to divide your paycheck between checking and savings accounts automatically 2. Schedule regular transfers – Set up recurring transfers from checking to savings accounts on paydays 3. Automate retirement contributions – Enable automatic 401(k)/IRA contributions through payroll or bank transfers 4. Enable round-up tools – Use apps that round purchases to the nearest dollar and save the difference

Automation Methods Comparison:

| Method | Best For | Setup Difficulty | Effectiveness |

|---|---|---|---|

| Direct deposit splitting | Regular income | Easy | Very high |

| Scheduled transfers | All income types | Easy | High |

| Round-up tools | Supplemental saving | Easy | Medium |

| Bill pay automation | Expense management | Medium | Medium |

| Tax-advantaged automation | Retirement saving | Medium | Very high |

Part 1: Setting Clear Savings Goals

Effective automation starts with knowing exactly what you’re saving for. Without specific goals, your savings lack purpose and direction.

Types of Savings Goals

Emergency Fund

- Typically 3-6 months of essential expenses

- Kept in high-liquidity, low-risk accounts

- Example: $15,000 in a high-yield savings account

Short-Term Goals (1-3 years)

- Vacations, weddings, vehicle purchases

- Kept in high-yield savings accounts or short-term CDs

- Example: $5,000 for a vacation in 12 months

Medium-Term Goals (3-10 years)

- Home down payment, education funds

- Mix of high-yield savings and conservative investments

- Example: $60,000 for a home down payment in 5 years

Long-Term Goals (10+ years)

- Retirement, financial independence

- Primarily investment accounts with growth orientation

- Example: $1.5 million for retirement in 30 years

Goal-Setting Framework

For each goal, define:

- Specific target amount

- Timeline for achievement

- Required monthly contribution

- Account type best suited for the goal

- Level of risk appropriate for the timeline

Example Goal Setup:

Goal: Emergency Fund

Target: $18,000 (6 months of expenses)

Timeline: 24 months

Monthly Contribution: $750

Account: High-yield savings account at 4.5% APY

Risk Level: Very low

Part 2: Choosing the Right Accounts

Different goals require different financial vehicles. Here’s how to match your goals with the appropriate accounts:

Emergency Funds & Short-Term Goals

High-Yield Savings Accounts (HYSAs)

- Benefits: FDIC-insured, liquid, competitive interest rates

- Recommended providers: Ally Bank (4.25% APY), Marcus by Goldman Sachs (4.30% APY), SoFi (4.50% APY)

- Automation features: Scheduled transfers, direct deposit splitting

Money Market Accounts

- Benefits: Sometimes higher interest than HYSAs, limited check-writing

- Recommended providers: Discover (4.15% APY), Capital One (4.25% APY)

- Automation features: Recurring transfers, automatic sweep options

Medium-Term Goals

Certificates of Deposit (CDs)

- Benefits: Higher fixed rates in exchange for term commitment

- Strategy: CD laddering (staggering maturity dates)

- Automation features: Automatic renewal options, interest reinvestment

Conservative Investment Portfolios

- Benefits: Potential for higher returns than cash accounts

- Options: 40/60 or 50/50 stock/bond allocations

- Automation features: Automatic rebalancing, recurring contributions

Long-Term Goals

Retirement Accounts

- 401(k)/403(b): Employer-sponsored, pre-tax contributions

- Traditional IRA: Tax-deferred growth, deductible contributions

- Roth IRA: Tax-free growth, after-tax contributions

- Automation features: Payroll deductions, automatic contribution increases

Taxable Brokerage Accounts

- Benefits: No contribution limits, high liquidity

- Providers: Vanguard, Fidelity, Charles Schwab

- Automation features: Recurring investments, dividend reinvestment

Part 3: Setting Up Your Automation System

Now that you understand your goals and account options, it’s time to build your automation system. Here’s a step-by-step approach:

Step 1: Optimize Direct Deposit

Split Your Paycheck

Most employers allow you to divide your direct deposit between multiple accounts. This is the most powerful automation tool available.

Example Setup:

- 70% to checking account (for bills and expenses)

- 15% to retirement accounts (401k)

- 10% to automated investment account

- 5% to high-yield emergency fund

Implementation:

- Contact your HR or payroll department

- Fill out a new direct deposit form specifying percentages or fixed amounts

- Provide account and routing numbers for each destination

Step 2: Schedule Regular Transfers

If your employer doesn’t offer direct deposit splitting, set up automatic transfers from your checking account instead.

Best Practices:

- Schedule transfers 1-2 days after your paycheck typically arrives

- Start with smaller amounts and gradually increase

- Align transfer frequency with your pay schedule

Example Setup:

- Transfer 1: $400 from Checking to Emergency Fund HYSA on the 1st and 15th

- Transfer 2: $250 from Checking to Vacation Fund HYSA on the 15th

- Transfer 3: $300 from Checking to Brokerage Account on the 1st

Step 3: Automate Retirement Contributions

Employer Plans (401k/403b)

- Set a fixed percentage of your income (aim for at least 15%)

- Enable automatic escalation (increases your contribution by 1% annually)

- At minimum, contribute enough to get full employer match

Individual Retirement Accounts (IRAs)

- Set up monthly automatic contributions from your checking account

- Divide annual contribution limit ($7,000 in 2025) by 12 = ~$583/month

- Schedule for beginning of month to maximize time in market

Step 4: Implement Round-Up Savings

Round-up tools automatically round purchases to the nearest dollar and save the difference. This creates an additional savings stream without any active management.

Popular Round-Up Services:

- Acorns: Invests your round-ups in diversified portfolios

- Chime: Transfers round-ups to your savings account

- Qapital: Offers customizable rules beyond simple round-ups

Example Impact:

With 30 transactions per week averaging $0.50 in round-ups: 30 × $0.50 × 52 weeks = $780 saved annually through round-ups alone

Step 5: Set Up Bill Pay Automation

Prevent late fees and credit damage by automating recurring bills:

- Fixed bills: Set recurring payments through your bank’s bill pay

- Variable bills: Set up auto-pay for the minimum due, then manually pay additional amounts

- Annual subscriptions: Create a dedicated “subscriptions” sinking fund with monthly contributions

Step 6: Enable Tax-Advantaged Automation

Many tax benefits require regular contributions to be most effective:

- HSA contributions: If eligible, set regular pre-tax contributions

- 529 College Savings: Schedule monthly transfers for education funds

- ESPP (Employee Stock Purchase Plan): Enable automatic payroll deductions

Part 4: Advanced Automation Strategies

Once you’ve mastered the basics, consider these advanced techniques:

Strategy 1: The “Save More Tomorrow” Approach

This behavioral finance technique helps increase savings rates without feeling the pain:

- Commit now to automatically increasing your savings rate with future raises

- Schedule contribution increases to coincide with expected salary increases

- Example: “I’ll increase my 401(k) contribution by 2% with each annual raise”

Implementation Example:

- Current salary: $60,000 with 10% retirement contribution

- After 5% raise to $63,000: Automatically increase to 12% contribution

- Result: Bigger retirement contribution without reducing take-home pay

Strategy 2: Automated Rebalancing

Keep your investment allocations on target without manual intervention:

- Choose investment platforms offering automatic rebalancing

- Set threshold-based rebalancing (when allocations drift by 5%+)

- Or schedule calendar-based rebalancing (quarterly/semi-annually)

Providers with Automated Rebalancing:

- Betterment

- Wealthfront

- Vanguard Personal Advisor Services

- Most target-date retirement funds

Strategy 3: Automated Tax-Loss Harvesting

Some platforms automatically capture tax benefits when investments decline:

- Services like Wealthfront and Betterment offer this feature

- Can improve after-tax returns by 0.5-1.0% annually

- Works automatically in the background

Strategy 4: Automated Debt Paydown

Apply automation to eliminate debt faster:

- Set up automated minimum payments on all debts

- Create additional automated payments to highest-interest debt

- As each debt is eliminated, automatically redirect that payment to the next highest-interest debt

Example System:

- Credit Card A: $100 minimum payment + $200 extra payment

- Credit Card B: $75 minimum payment

- Student Loan: $300 minimum payment

When Credit Card A is paid off, automatically redirect $300 to Credit Card B

Part 5: Tools and Apps for Savings Automation

Banking Tools

Online Banks With Strong Automation:

- Ally Bank: Recurring transfers, “buckets” for different goals

- Capital One 360: Automatic savings plans, multiple account creation

- SoFi: Roundups, competitive interest rates, “vaults” for goals

Dedicated Savings Apps

- Qapital: Rule-based automated savings with IFTTT integration

- Digit: AI-powered savings that analyzes spending patterns

- Albert: Guided financial automation with smart savings

Investment Automation

- M1 Finance: Automated investing with customizable “pies”

- Betterment: Goal-based automated investing with tax optimization

- Fidelity Go: Low-cost automated investing with fractional shares

All-In-One Financial Tools

- Personal Capital: Comprehensive dashboard with investment automation

- YNAB (You Need A Budget): Budgeting with scheduled transaction management

- Rocket Money (formerly Truebill): Bill management and savings automation

Part 6: Optimizing Your Automated System

Quarterly Review Process

Schedule calendar reminders to review your automation system quarterly:

- Evaluate Goals: Are your targets still relevant?

- Assess Performance: Are you on track? Do contribution amounts need adjustment?

- Check Interest Rates: Are your accounts still competitive?

- Review Fees: Are there lower-cost alternatives?

- Optimize Tax Efficiency: Are you maximizing tax-advantaged accounts?

Annual Optimization

Once yearly, perform these deeper adjustments:

- Increase Contribution Rates: Try to raise savings by at least 1%

- Update Risk Allocations: Adjust as goals approach or life circumstances change

- Tax-Advantaged Account Review: Ensure you’re maximizing available tax benefits

- Insurance Integration: Align insurance coverage with accumulated assets

Life Event Triggers

Certain events should prompt immediate system updates:

- Income changes: Adjust contribution amounts proportionally

- Marriage/divorce: Consolidate or separate automated financial systems

- Children: Add college savings automation

- Home purchase: Redirect former rent payment amount to savings/investments

- Job change: Update retirement plan automation

Part 7: Common Challenges and Solutions

Challenge: Unpredictable Income

For freelancers or those with variable income:

Solution: Create a “stability buffer” in checking, then use percentage-based transfers:

- Set a baseline checking account target (e.g., $3,000)

- Any amount above this triggers an automatic transfer of 40% to savings/investments

- During low-income periods, automation pauses until checking rebuilds

Challenge: Avoiding Over-Automation

Too much automation can lead to disengagement or overdrafts.

Solution: Implement safety nets:

- Maintain a cash buffer in checking ($500-1,000 above monthly needs)

- Set up low-balance alerts (get notified when checking falls below threshold)

- Schedule monthly “financial check-ins” to maintain awareness

Challenge: Emergency Access to Funds

What if you need quick access to automated savings?

Solution: Create a tiered emergency system:

- Checking account buffer for smaller emergencies

- High-yield savings account for medium emergencies

- Roth IRA contributions (not earnings) can be withdrawn penalty-free

- Only in extreme cases, access other investments

Conclusion: Your Personalized Automation Plan

The most effective automation system aligns with your unique financial situation, goals, and personality. Use this guide to create a customized plan that works for you.

Key Steps to Implementation:

- Start with clear financial goals

- Choose the right accounts for each goal

- Set up direct deposit splitting if available

- Establish automatic transfers on payday

- Enable retirement account automation

- Add round-ups and other micro-saving techniques

- Review and optimize regularly

Remember that automation is not set-and-forget forever. Life changes, financial goals evolve, and your system should adapt accordingly. Schedule regular reviews but otherwise let your automated system quietly build your wealth in the background.

By automating your savings, you’re not just building financial security—you’re buying freedom, options, and peace of mind for your future self.